What the heck is “Neoclassical Economics”?

What the heck is “Neoclassical Economics”?

TLDR: “Neoclassical economics” is taught to thousands of new, unsuspecting economic students globally every year. We introduce one of its core components: supply and demand curves. But we also point out that these seemingly innocuous curves are built on the corrosive principles of unbridled self-interest and maximization of profit and pleasure (or “utility” as neoclassical economists call it), and are the culmination of a centuries-long campaign to strip economics of all ethical content. We show how neoclassical economists hide all this behind a veneer of mathematics.

Supply and Demand Curves: A Core Teaching of Neoclassical Economics

Let’s begin by introducing you to the antagonist of this newsletter, which is a theoretical construction called “neoclassical economics.”

Every year, thousands of introductory economics students worldwide crack open their shiny new textbooks, keen to learn how economies work.

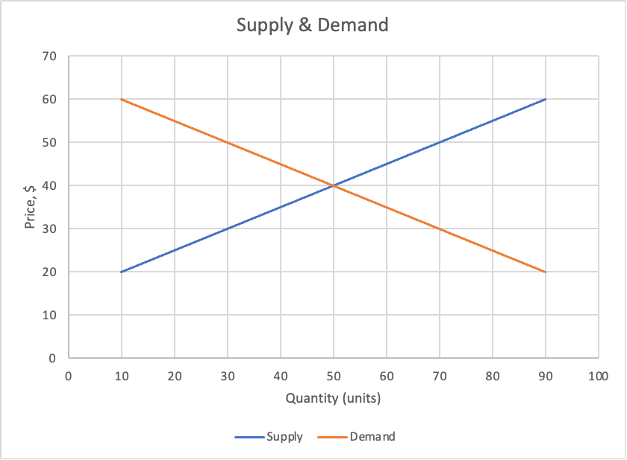

Within days of their courses beginning , their professors shall show these eager students a graph that looks something like this:

Very quickly, the students will begin calling these “supply and demand curves.” Or perhaps more formally, “market equilibrium graphs,” or occasionally a “Marshallian cross,” after the late 19th century British economist Alfred Marshall who invented them.

Students shall often be told, decisively, that this graph explains “how markets work.”

The vertical, or “y-axis” represents price. The horizontal, or “x-axis,” represents quantity. Within the graph, the line that slopes up and to the right is called “the supply curve.” The line that slopes down and to the right is called the “demand curve.”

Together, these lines depict the intuitively powerful and seemingly air tight relationship between the supply of a good or service, the demand for it, and its price; both the price consumers are willing to pay for that good or service, and the price at which suppliers are willing to produce and sell it.

Simply put, as the price of a good goes up, suppliers are willing to produce more and more of it. Yet at the same time, as that price rises, consumers will demand less and less of it. In other words, as prices go up, demand goes down, and vice versa. The point at which the two curves intersect is called the “equilibrium price,” or “market price.” In our example, at $40, 50 units will be demanded, and 50 units supplied. Supply is thus theoretically matched perfectly with demand, and we are witness to the idyllic state economists call “market equilibrium.”

What influences demand for a good, other than the price itself? Variable such as income, taste, expectations, the price of similar goods, and the number of buyers in the market, students shall be taught.

What influences sellers of a good, other than the price itself? Variables such as the cost of inputs, technology, expectations, and the number of sellers in the market, students shall be taught.

What Introductory Economic Students are Never Told

My own first encounter these graphs and theories came during the second semester of my freshman year at Boston University. On the advice of a formidable undergraduate advisor, I enrolled in “Introductory Microeconomics.” I thus had my first contact with market equilibrium and other core tenets of a modern economics education.

I was immediately enthralled. Economics textbooks are filled with graphical depictions of every day transactions of production and exchange. Though much of what underlay these graphs made simple, intuitive sense - such as the law of supply and demand we just saw - there was something elegant, logical and precise in the way economists explained. I dutifully copied these graphs into my notebooks, learned the laws and formulas, and ended up making economics the second of my two undergraduate majors.

Now, decades later, I have come to understand that the way I was taught economics – and the way it continues to be taught to thousands and thousands of economic students even today - is manipulative, deceptive, misleading and even harmful to our collective consciousness.

Deceptive Mathematics…

For starters, I was likely not told that this simple supply and demand graph, as well as many other core tenets of a modern microeconomics* textbook were part of a theoretical approach to economics called “neoclassical.”

Even today, most economics students receive no training in the history of the craft; economic history is mostly considered irrelevant.

Instead, the unspoken message was that economists spoke truth. The fact that they invoked mathematics to make their case, only bolstered that perception.

Yet I was never told that the way neoclassical economists use mathematics was fundamentally different than the way it is used in other sciences. The way math is used in economics is not the same way math is used in physics, to help us understand how the universe works; nor as it is used in engineering, to build homes and vital infrastructure; nor as it used to bring financial order to business, as accounting does.

Instead, neoclassical economists use math solely to prove the tenets of the self-contained, sealed-off, imaginary, and completely theoretical world of neoclassical economics.

…and Delusional Engineers

Imagine if a group of delusional engineers had built an airplane that could never fly, but could fly in theory, if only we assumed the engine worked, the wings worked, and it had landing gear. The conversation might go like this.

Delusional Engineer: “Assume the engine on this airplane works.”

Student: “But it doesn’t.”

Delusional Engineer: “Just assume it does. Also, assume that the wings provide lift.”

Student: “But they don’t.”

Delusional Engineer: “Just assume they do.”

Delusional Student: “But they don’t.”

Delusional Engineer: “I know, I know. But just assume they do. And assume the fuselage can withstand the air pressure above 1,000 feet.”

Student: “But it can’t.”

Delusional Engineer: “Yes, I know. Assume it can. Now if you just ignore real life and assume all those things work in theory, this airplane flies!”

This is how math is put to work in neoclassical economics: in a purely theoretical way, so that economists can talk to other economists. It is an approach to economics that is completely severed from the real world.

But I was not told this.

Nor was I taught that many of the foundations of neoclassical economic theory had been criticized time and time again, by economists themselves.

And I most certainly was not told that neoclassical economics was the result of a purposeful campaign, waged by economists over more than two centuries, to strip economics of all ethical content.

This is so important to the message of this newsletter, that I will repeat it: the simple, logical-seeming supply and demand graph, which is at the beating heart of how economics is taught to hundreds of thousands of students world-wide today, is the culmination of a committed crusade by economists to strip economics of all ethical content.

For within that graph are hidden two of the corrosives, foundational assumptions in neoclassical economics: self-interest, and maximization.

The Corrosive “Self” in Neoclassical Self-interest

Neoclassical economics claims that people and companies are driven solely by self-interest.

Or rather, consumers and companies.

For in mainstream economic theory we are not people. We are consumers. As consumers, we care about consumption and little else. Gone in these economic models are our deepest values, our ethical make up, our “higher selves.” To these economists, we have no consciousness, no compassion, no empathy, nor concern for others’ well-being, and certainly no spiritual essence. As mindless as sharks, we are infinitely ravenous creatures, seeking only satiation.

In this world, consumers and companies seek only to “maximize.” Companies seek to maximize profits, while consumers seek to maximize “utility,” a fictitious proxy for pleasure in theoretical economics.

Further, economists consider such maximization to be “rational.” Economists define rationality as “maximization of utility (pleasure) and profits.”

Of course, this idea is completely absurd. Maximization, as defined by economists, is not rational at all. It is a form of delusion.

The reason is simple: if all us humans simultaneously pursued maximization as described by economists, the only possible outcome is conflict, either with other people, the sustainable limits of the planet, or with one’s own sense of morality. For at some point, my pursuit of maximization will clash with your pursuit of maximization and discord shall emerge.

Economists handle this obvious objection (that the unbridled pursuit of “maximization” can only lead to conflict) with a combination of theoretical magic tricks.

For example, the lack of money puts a limit, or constraint, on how much you can maximize; this is called the “budget constraint,” as first year economics students are taught.

But the most commonly cited illusions are the ostensible utopic benefits of the pursuit of “self-interest,” combined with the “free market.”

(More recently, economists have added “behavioral economics” to this bag of magic tricks. Ostensibly, behavioral economics incorporates “psychology” into the craft; but later in this newsletter, I’ll show that this is only a tiny bit true. Instead, behavioral economists often lend their considerable prestige to the mundane task of getting people to buy more stuff, while the founding fathers of the field all advocate on behalf of perpetuating neoclassical economics, with its commitment to self-interest and maximization of pleasure and profit).

Per this magical theoretical panacea, the business owner, motivated by self-interest, seeks a profit; in pursuing such profit she will pay salaries to self-interested workers and purchase inputs from other self-interested businesses. Thus, the pursuit of self-interest spawns job-creation and the production of goods and services that satisfy consumer needs and uncorks a virtuous cycle of economic and employment growth.

As this theoretical, virtuous cycle unfolds, prices are set by the interaction of supply and demand in the free market. Eventually, supply and demand are in balance, and both individual industries and the entire economy reaches equilibrium.

Furthermore, is not “self-interest” nearly synonymous with other worthy personal quests, such as self-help, self-esteem, self-awareness and self-discovery?

In certain circumstances, the answer may well be “yes.” But not in economics. For in neoclassical economics, the theoretical “self” pursuing its interests, is an extremely reduced version of, say, my complete “self” or your complete “self.”

It is an atomistic , individualistic “self” who exists largely in isolation, severed from all human connection, maximizing pleasure and profit in a hyper-competitive marketplace, with no concern for consequence.

According to economists’ version of “self,” we are not allowed to care for our neighbor in her hour of need; nor tend to the sick, nor the poor or dying. It is a “self” stripped of our highest and most noble values.

This is because neo-classical theory does not allow any offsetting values, such as compassion, generosity, temperance or loving-kindness, to offer their tempering balm, when our pursuit of self-interest results in unintended harm.

Instead, in the theoretical world of neo-classical economics, our entire focus, every iota of our theoretical being, must be focused solely on material accumulation.

But I was told none of this in my introductory economics courses. Nor are students told this today, as year upon year, thousands upon thousands begin their introductory studies in economics.

----

*“Micro” economics studies how small economic units such as individuals, households, companies or industries interact with one another. “Macro” economics looks at a bitter picture, such as the workings of national economies, or how countries trade with one another.

Further reading:

Any introductory economics or microeconomics textbook, such as N. Gregory Mankiw’s, Principles of Microeconomics, 8th ed. , Cengage Learning, Boston MA, 2018.

Quotes Critical of Economics: https://weapedagogy.wordpress.com/2018/07/26/quotes-critical-of-economics/